Rent To Own vs. Renting: Which Builds More For Your Family?

- The Table.

- May 26

- 5 min read

Both involve a monthly payment. Only one of them is building something you'll own. Here's the side-by-side most renters in Ocala have never been shown.

Every month, more than half of Ocala households write a rent check. The average one is $1,549 — up 3.49% from last year. (Source: RentCafe / Yardi Matrix, 2026)

That money goes somewhere. The question most renters don't ask out loud is: where, and for whose benefit?

This article puts renting and rent to own next to each other. Same family, same monthly budget, same Ocala market, and shows you what each one is actually building.

What You're Actually Paying For

When you rent in Ocala

You pay your landlord every month. In exchange, you get:

A place to live

The landlord's promise to handle major repairs

The right to stay until your lease ends

You don't get:

Equity

A locked purchase price

A path to owning the home you live in

Protection from rent increases when your lease renews

When the lease ends, you have the same thing you had at the start: a place to live, until the next lease. The money is gone. The landlord owns the asset that you helped pay for.

When you rent to own in Ocala

You pay a monthly amount that's typically higher than market rent (because it includes an ownership credit). In exchange, you get:

A place to live

A locked purchase price for the home, set the day you sign

A monthly ownership credit (typically $250–$500) that accrues toward your down payment

Your upfront option fee ($9,000–$17,000) credited toward your purchase at closing

The exclusive right to buy the home at the end of the lease term

Time (1–3 years) to build credit, save, and qualify for the best possible mortgage

When the lease ends, you have a choice that a renter never gets: close on the home at the locked-in price, or walk away.

Side-By-Side: Where Your Money Goes

Let's run the same family through both scenarios over 24 months. Mid-range Ocala numbers.

Renting | Rent To Own | |

Monthly payment | $1,800 | $2,400 |

24-month total paid | $43,200 | $57,600 |

Upfront cost | First/last/security (~$5,400) | Option fee (~$13,000) |

What's building toward ownership | $0 | Option fee + monthly credits (~$13,000 + $9,600 = $22,600) |

End of 24 months — you have | A place you lived | A locked purchase price + $22,600 already applied + time used to qualify for a mortgage |

Equity built | $0 | Up to $22,600 + market appreciation if you buy |

The renter paid $43,200 over 24 months and walks away with nothing.

The rent-to-own family paid $57,600, but $22,600 of it is theirs. They're walking into closing with that money already applied to the home.

That's a $14,400 difference in monthly outlay over two years, and a $66,000+ difference in net position (because the locked price also protects them from market appreciation).

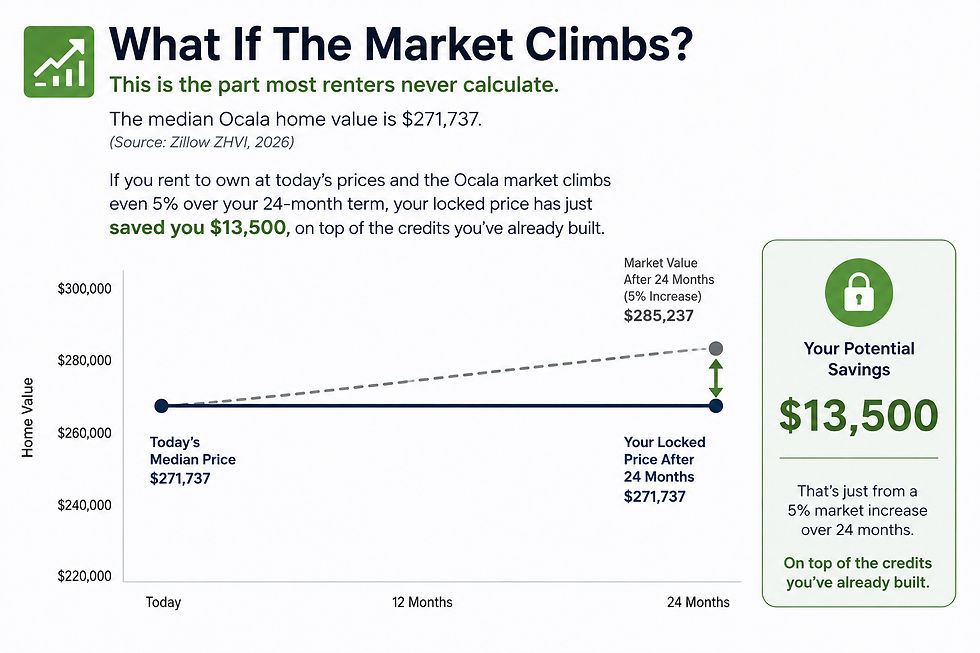

What If The Market Climbs?

This is the part most renters never calculate.

The median Ocala home value is $271,737. (Source: Zillow ZHVI, 2026)

If you rent to own at today's prices and the Ocala market climbs even 5% over your 24-month term, your locked price has just saved you $13,500, on top of the credits you've already built.

If the market stays flat, you still keep your credits.

If the market drops, you have a choice: buy at the locked-in price anyway (because you love the home), or walk away.

In all three scenarios, the rent-to-own buyer has options the renter doesn't.

When Does Renting Make More Sense?

We're a rent-to-own brokerage. We're also going to tell you the truth.

Renting is the right call if:

You're not sure you'll be in Ocala in two years

You don't have the upfront option fee saved

Your job situation is unstable enough that a 1–3 year commitment doesn't fit

You're not emotionally ready for the responsibilities of ownership (yard, maintenance, taxes, insurance)

You're actively in a major life transition (divorce, job change, family change)

If any of those describe you right now, rent. Save. Come back when the timing fits.

Rent to own is the right call if:

You're tired of paying someone else's mortgage

You have steady income (typically $75K+ household) but your credit isn't quite ready for a traditional mortgage

You have $9K–$17K available for an option fee

You plan to stay in Ocala or Marion County for at least 2+ years

You want to lock today's price before the market climbs further

If most of those describe you, the math favors rent to own. Significantly.

The Hidden Cost Of Waiting

Here's the calculation most renters never make.

In Ocala, average rent climbed 3.49% in the past year alone. (Source: RentCafe, 2026)

If you keep renting for two more years at $1,800/month, and your landlord raises rent 3.5% per year (which is conservative), you'll pay:

Year 1: $21,600

Year 2: $22,356

Total: $43,956 over 24 months, and your rent next year is $1,932

That same family on the rent-to-own path locked in their housing cost at $2,400/month for 24 months. No surprise rent increases. Predictable monthly outlay. And $22,600 of that going toward ownership.

The "cheaper" path of renting is only cheaper on paper. Once you account for what you're not building, it's the more expensive path.

What This Looks Like For A Real Ocala Family

The Martinez family came to us with a familiar story: steady income, two kids, renting for years, told by every bank that their credit wasn't ready. They signed a 24-month rent-to-own agreement on a home in Freedom Crossing.

"We never thought we could own a home with our credit situation. Rent to own gave us 1-3 years to rebuild, and now we're closing on our home in Freedom Crossing." — The Martinez Family, Ocala FL

That's the difference between paying rent and paying toward something. Same monthly check. Different outcome.

Which Path Is Right For Your Family?

The honest answer is: it depends on your situation. Income, credit, savings, timeline, family plans.

The fastest way to know is to take 60 seconds and see if the path is open to you. No credit pull. No commitment. We'll tell you plainly whether rent to own fits your family — and if it doesn't, we'll tell you that too.

Related Articles (Internal Links Section)

How Does Rent To Own Work In Ocala, FL? A Complete Guide →

What To Ask Before Signing Any Rent To Own Agreement →

Last updated: May 2026. Cost comparisons are illustrative based on average Ocala market data and typical Rent To Own Ocala agreement structures. Individual terms vary by property and buyer qualification. Rent To Own Ocala is operated by The Table Brokerage, a licensed Florida real estate firm.

SOURCES CITED (for editorial review)

RentCafe / Yardi Matrix, "Average Rent in Ocala, FL: 2026 Rent Prices by Neighborhood," Feb 2026

Point2Homes, "Average rent in Ocala | Rental Housing Market 2026," 2026

Zillow, "Ocala, FL Housing Market: 2026 Home Prices & Trends," April 2026

Comments